Table of Content

Interest rates and house prices can impact your decision to buy a home. However, your personal and financial positions play a more critical role when becoming a homeowner. Over 35 years ago, Optiver’s business started with a single trader on the floor of Amsterdam’s European Stock Exchange. Since our 1986 founding, Optiver’s Amsterdam office has grown into one of the most dynamic and exciting trading floors in Europe. Our culture reflects the Dutch capital city’s progressive, innovative and inclusive nature. With its unique spirit, Amsterdam is the ideal hub for our teams to trade a wide range of products from listed derivatives to cash equities, ETFs, bonds and foreign exchange.

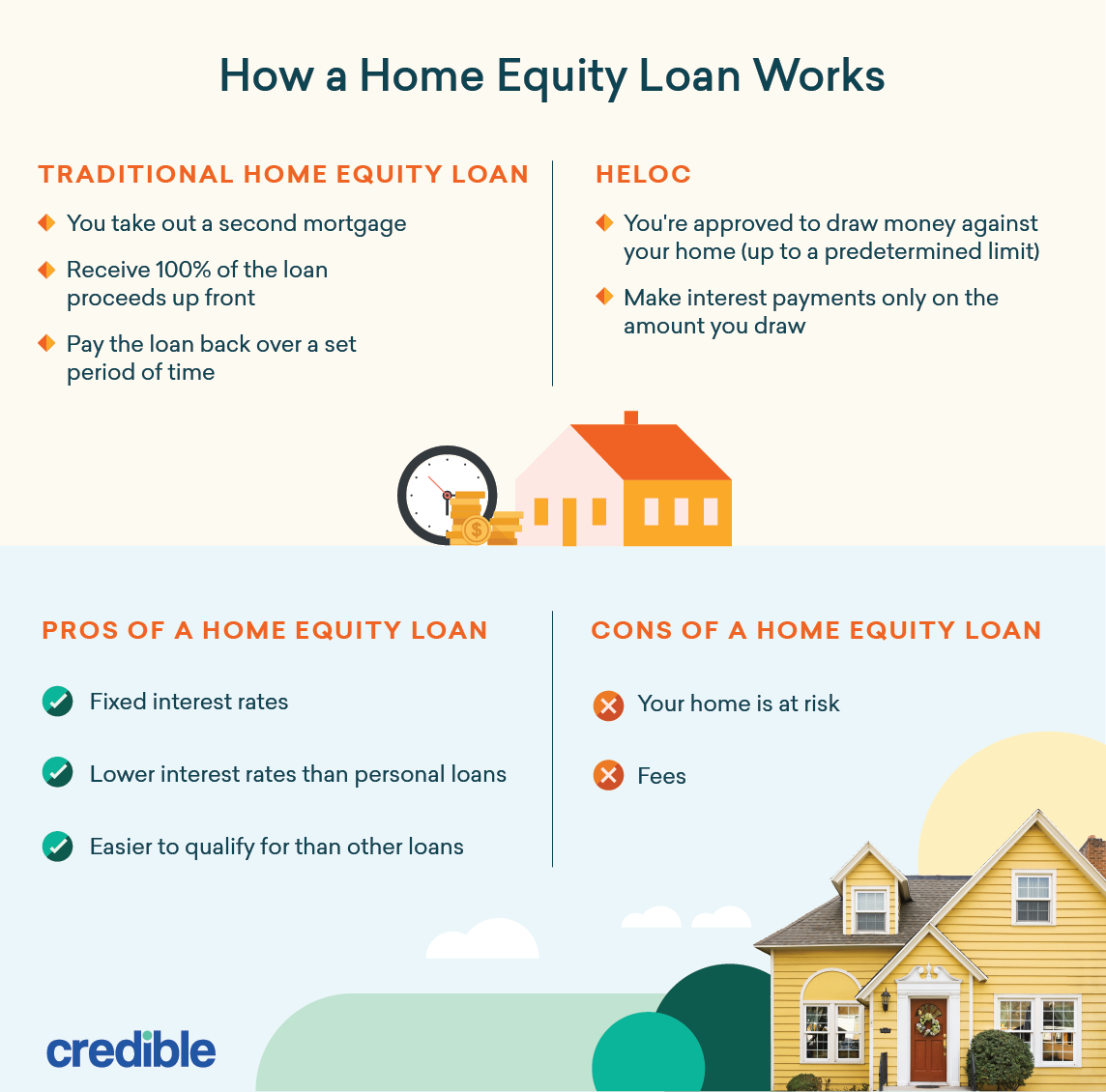

With a home equity loan, you’ll receive a lump sum payment that you can deposit in your bank account and use as needed. Your lender will provide a monthly repayment schedule, including principal and interest, and the loan’s term. Most lenders will allow you to borrow anywhere from 15% to 20% of your home's available equity. To calculate your home equity, subtract your remaining mortgage balance from the current appraised value of your home. How much equity a bank or lender will let you take out depends on a number of additional factors such as your credit score, income and DTI ratio. For most homeowners, it can take five to 10 years of mortgage payments to build up enough tappable equity to borrow against.

Access more of your home equity with Lower.

Understand how your home equity financing will affect your taxes and whether you may qualify for any tax advantages. To ensure you get the most out of the equity you’ve built in your home, follow a few best practices when considering taking out a home equity loan or HELOC. Because the home is used as collateral, you may risk foreclosure if you can’t repay the loan.

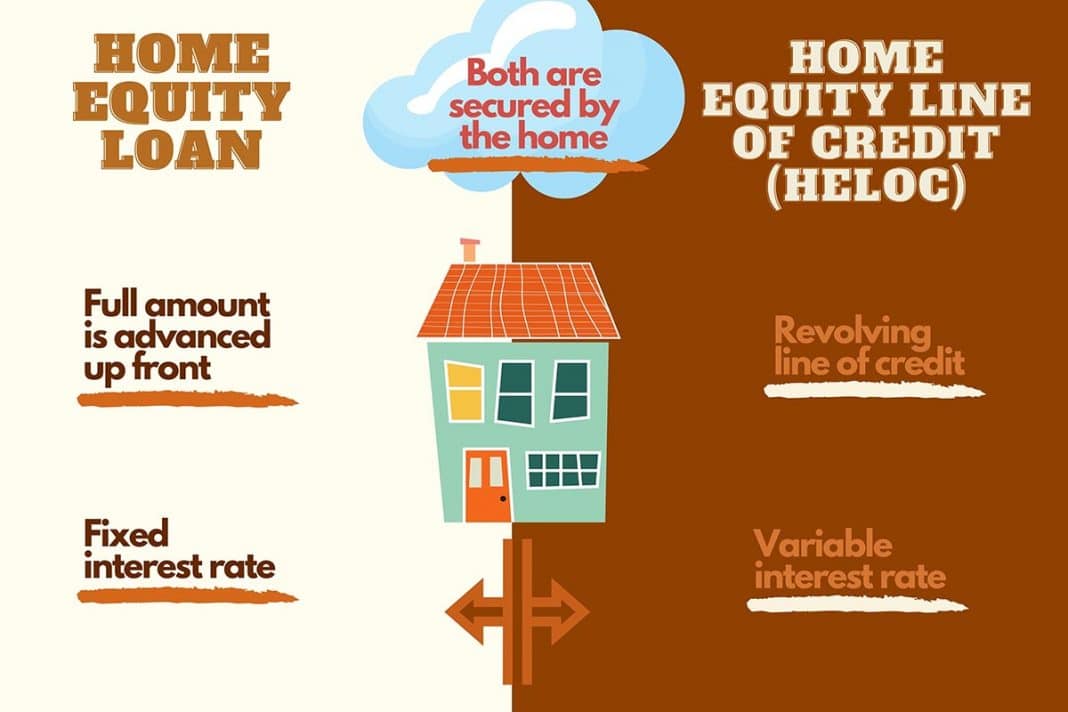

A home equity loan is essentially a second mortgage you take out against your home and can be used to fund major life expenses like home renovations and college tuition. Home equity loans have fixed-interest rates which makes them an attractive loan product as interest rates continue rising and inflation persists. Home values have risen substantially over the past two years, making home equity loans -- which provide you with a lump sum of cash at a fixed interest-rate -- an appealing option for many. A fixed rate comes with steady payments for the life of the loan.

Editorial disclosure:

You take out a new mortgage for more than you owe on the existing one, and you get the difference to use for your expenses or projects. As of July 27, 2022, the average annual percentage rate for a 30-year fixed-rate mortgage was 5.61%. Home equity loans are usually more expensive than mortgages. The customer service team is available Monday through Thursday from 9 a.m.

If you can’t get better terms or a lower interest rate than what you have on your existing debt, keep looking at what other lenders offer. Having a plan for how you’ll attack high-interest debt — and how you’ll repay your home equity loan — can set your finances up for a more secure future. Generally, you’ll need a credit score of at least 620 to qualify for a home equity loan, but some lenders offer this type of loan even if you have a lower score or bad credit. This assumes, however, that you have adequate equity in your home and a lower debt-to-income ratio, preferably under 43 percent. If you’re seeking a home equity loan to consolidate debt, the latter might not add up for you. One option is to work with the lender that originated your first mortgage as you already have a relationship and history of on-time payments.

Equity in health care prioritisation: an empirical inquiry into social value.

That's what happened to millions of Americans during the2008 financial crisis. Today, however, there's less risk of your home's value decreasing below your home equity loan amount. Home prices have appreciated more than 40% across the US since the beginning of the pandemic, and it seems unlikely that they'll go down in a significant way anytime soon. For example, if you have a $500,000 mortgage and you owe $350,000 on it, you have $150,000 in equity.

A home equity loan, which lets you borrow money against the equity you've built in your home, provides you with a lump sum of cash at a fixed interest rate. Mortgages can have lower interest rates than home equity loans, but that doesn’t mean they’re always a better choice. When deciding which loan type is best for you, consider your goals, credit, and current loan terms. Keep in mind that the rates for home equity loans and mortgages are always changing, so it’s important to shop around with multiple lenders to find the latest rates.

Extending the term of your loan means lower monthly payments, which can free up some money if you have a tight budget. Monthly payments on a 10-year fixed-rate refi at 5.97 percent would cost $1,108.70 per month for every $100,000 you borrow. That's a lot more than the monthly payment on even a 15-year refinance, but in return you'll pay even less in interest than you would with a 15-year term. With a home equity loan, you receive the entire loan amount as a lump sum payment with repayment terms set to a fixed interest rate over a specified length of time.

That can mean higher interest rates paid on deposit accounts and lower ones charged on loans. Home equity loans are available from many banks, credit unions, and online lenders. If your credit score is less than 500, work on improving it before applying for a mortgage, because most lenders won’t issue a loan to someone with a score of 499 or lower. On the other hand, if your credit score is higher than these minimums, you may be able to secure a better interest rate. Shopping around is crucial to get the best deal on your mortgage. Make sure to get quotes from at least three lenders, and pay attention not just to the interest rate but also to the fees they charge and other terms.

To calculate the percentage, divide $150,000 by your home's value of $500,000 and you'll have 30% of equity available in your home. Lenders will typically let you borrow around 80% to 85% of your home's equity for a home equity loan. So, in this example, you can borrow up to $120,000 to $127,500.

Applications without a letter of motivation will not be reviewed. When we think there is a potential match, you will hear from us sooner than you expect. If you have any questions feel free to contact our Recruitment team at Please note, we cannot accept applications via email for data protection reasons. Sign Up NowGet this delivered to your inbox, and more info about our products and services. Mortgage applications to purchase a home rose 4% for the week and were 38% lower than the same week one year ago. That annual comparison is now shrinking slightly as rates drop.

HELOCs also have variable interest rates, which means your monthly payments will go up and down depending on interest rate trends. A home equity loan offers you predictable monthly payments because your interest rate is fixed and never changes. You are on a set repayment schedule and will make the same monthly payment for your whole loan term. Since home equity loan lenders rely on your home’s current value to determine how much you can borrow, you might need to pay for an appraisal. If you have a lot of debt to consolidate, paying these extra fees might still make sense, but it’s wise to compare the fees you would have to pay with the amount you’d ultimately save in interest.

They had good technology in place for review and signing of documents. The coordination to make sure I was kept informed was very good. I would definitely recommend them and have recommended my agent to others who would be interested in refinancing.

If you are a first-time customer with Lower, you can expect fees to be at least $1,500. But if you already have a loan with Lower, the company waives the lender fees on any refinance. So, if you take out a second loan through Lower, you won't have to pay any origination, underwriting, processing or administrative fees. You'll want to consider what type of financial institution best suits your needs. In addition to mortgage lenders, financial institutions that offer home equity loans include banks, credit unions and online-only lenders.

No comments:

Post a Comment